“Today’s investments might seem all about quick returns and flashy trends, but have you ever thought about the classic strategies that built real wealth over time?

Remember dreaming of being a millionaire someday?

Starting to invest in your twenties can make that dream come true. Stay tuned, and we’ll explore how you can turn those dreams into reality with smart financial decisions.”

“Forget get-rich-quick schemes and short-term fixes! We’re looking into the essentials of investing, from building a strong financial foundation to exploring stocks, real estate, mutual funds, and more. You’ll learn how to build long-term wealth with patience and the right strategies.

1: Understanding the Basics of Investing

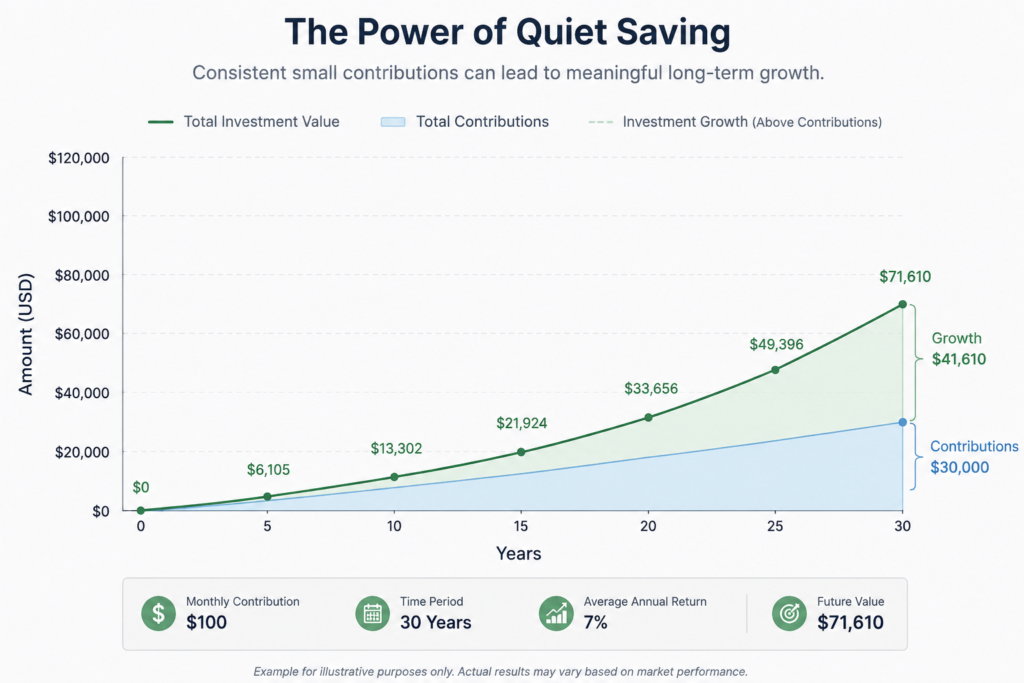

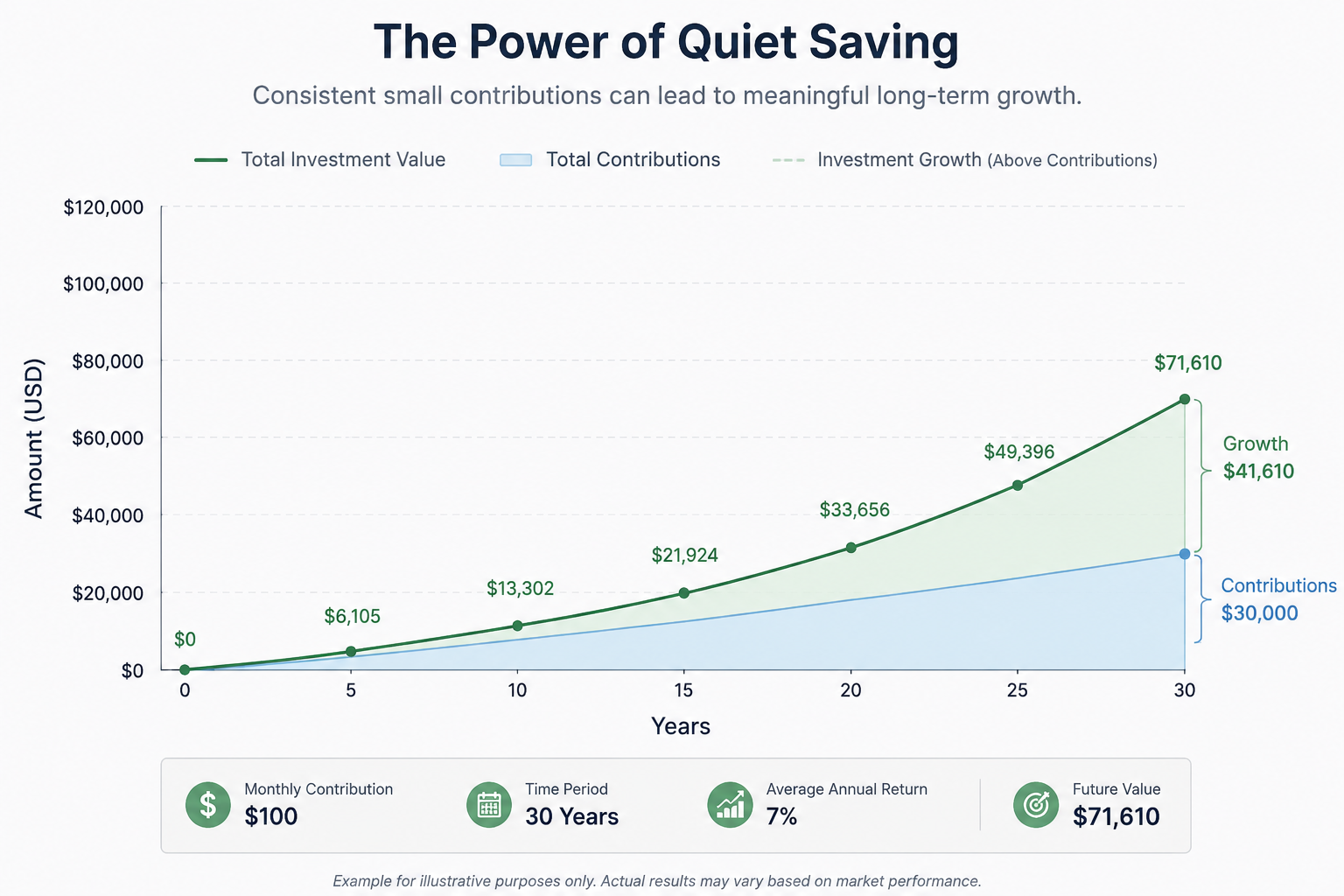

“Starting to invest can seem daunting, but it’s one of the best decisions you can make for your financial future. The key is to start early and let your money grow over time.”

“Investing early allows your money to grow over time, thanks to the magic of compound interest. Compound interest is like a snowball effect—your initial investment earns interest, and then that interest earns interest, and so on. The earlier you start, the more powerful this effect becomes.”

“For example, let’s say you start investing just $100 a month at age 20. With an average annual return of 7%, by the time you’re 60, you could have over $300,000. That’s the power of compound interest working for you! Imagine reaching retirement age with a significant nest egg simply because you started early and stayed consistent. Think of it like planting a tree—the sooner you plant it, the more time it has to grow and bear fruit.”

2: Stocks

“One of the most well-known and potentially rewarding ways to invest is by buying stocks. But what exactly are stocks, and how do they work?”

“Stocks represent ownership in a company. When you buy a stock, you own a small part of that company. This means you have a claim on part of the company’s assets and earnings. Stocks are traded on stock exchanges, and their prices can fluctuate based on the company’s performance and market conditions.”

“Historically, stocks have offered higher returns compared to other investment options like bonds or savings accounts, but they also come with higher risks. The value of stocks can go up and down, sometimes dramatically, so it’s important to be prepared for volatility.”

“Consider investing in well-known companies like Apple or Google, which have shown significant growth over the years. For instance, if you had invested $1,000 in Apple stock in 2000, your investment would be worth over $50,000 today. While not every stock will perform like Apple, investing in solid companies with strong growth potential can significantly increase your wealth over time.”

3: Real Estate

“Real estate is another solid investment option that offers unique benefits. But is it the right choice for you?”

“Real estate investments involve purchasing property to generate rental income or to sell at a higher price. This can include residential properties like houses and apartments, commercial properties like office buildings, or even land. Real estate can be a stable investment, providing both income from rent and potential appreciation in property value over time. It’s a tangible asset that often increases in value, especially in growing neighborhoods or cities. Plus, real estate investments can offer tax benefits, such as deductions for mortgage interest and property depreciation.”

“Think about buying a rental property in a growing neighborhood. For instance, imagine purchasing a duplex in an up-and-coming area. You can rent out one unit to cover your mortgage and expenses while living in the other unit. Over time, as the neighborhood develops, property values are likely to increase. This setup not only provides you with a steady income from rent but also allows your property to appreciate in value, giving you the option to sell it at a higher price later. It’s like planting a seed in fertile soil and watching it grow into a fruitful tree.”

4: Mutual Funds and ETFs

“Next, let’s talk about mutual funds and ETFs, which are fantastic tools for diversifying your investment portfolio.”

“Mutual funds pool money from many investors to invest in a diversified portfolio of stocks, bonds, or other assets. They are managed by professional fund managers who allocate the fund’s investments to meet the fund’s objective. This diversification helps spread risk because the fund is invested in a wide variety of assets rather than relying on the performance of a single investment. Mutual funds can be actively managed, where the manager makes decisions about how to allocate assets, or passively managed, tracking an index like the S&P 500.”

“ETFs (Exchange-Traded Funds) are similar to mutual funds but trade like stocks on an exchange. They combine the diversification benefits of mutual funds with the flexibility of stock trading. ETFs can track a wide range of indices, commodities, or sectors, providing a simple way to gain exposure to a broad market or specific niche.”

“Investing in an S&P 500 ETF gives you exposure to the top 500 companies in the U.S., spreading your risk across many different stocks. For example, if you buy shares of an S&P 500 ETF, you’re indirectly investing in companies like Apple, Microsoft, and Amazon. This means that even if one company underperforms, the strong performance of others can help balance your overall returns. It’s like having a basket of fruit; even if one apple goes bad, you still have a variety of other fruits that are perfectly fine.”

5: Creating a Budget and Financial Plan

Introduction: “Creating a budget is the foundation of any good financial plan. It helps you understand where your money is going and ensures you save enough for your investment goals.”

“Start by listing all your sources of income and then categorize your expenses into fixed (like rent and utilities) and variable (like dining out and entertainment). This gives you a clear picture of your financial situation. Next, set aside a specific amount each month for investing. Treat this amount as a non-negotiable expense, just like paying your rent or utility bills. Automating your savings can help make this process easier and ensure you consistently invest every month.”

Example/Story: “If you earn $3,000 a month, try to save at least $300 for your investment fund. By setting aside 10% of your income, you’ll be able to build a solid investment portfolio over time. Think of it like paying yourself first—prioritizing your financial future over immediate wants. It might require some adjustments initially, but the long-term benefits are well worth the effort.”

6: Building an Emergency Fund

Introduction: “Before looking into investments, it’s important to have an emergency fund in place. This fund acts as a financial safety net for unexpected expenses.”

“An emergency fund should cover three to six months’ worth of living expenses and be kept in a high-interest savings account. This way, your money is easily accessible and continues to earn interest. Having an emergency fund provides peace of mind, knowing you’re prepared for unexpected expenses, such as medical emergencies, car repairs, or sudden job loss. It prevents you from dipping into your investments and allows them to grow uninterrupted.”

“Imagine you suddenly face a large, unexpected expense like a medical emergency or car repair. Without an emergency fund, you might have to sell your investments at a loss to cover the costs. But with a well-funded emergency account, you can handle these situations without disrupting your long-term investment goals. This financial buffer not only protects your investments but also helps you sleep better at night, knowing you’re prepared for whatever life throws your way.”

Section 7: Long-Term Investment Strategies

“Now that we’ve discussed the importance of having an emergency fund let’s explore long-term investment strategies that can help you build lasting wealth.”

“Investing for the long term allows you to ride out market volatility and benefit from overall market growth. The stock market can be unpredictable in the short term, with prices fluctuating due to various factors. However, over the long term, the market has historically trended upwards, rewarding patient investors. This means that even if the market dips temporarily, staying invested can help you recover and profit from future gains.”

“Avoid trying to time the market; instead, focus on consistent, regular investments. Timing the market, or trying to buy low and sell high, is extremely difficult even for experienced investors. Instead, adopt a strategy known as dollar-cost averaging. This involves investing a fixed amount of money at regular intervals, regardless of market conditions. This approach reduces the risk of making poor investment decisions based on short-term market movements and ensures that you continue to build your portfolio over time.”

“Dollar-cost averaging can help mitigate the impact of market fluctuations. For example, let’s say you invest $200 every month in a mutual fund. When the market is down, your $200 buys more shares. When the market is up, your $200 buys fewer shares. Over time, this strategy averages out the cost of your investments, potentially lowering your overall cost per share and reducing the impact of market volatility. By consistently investing, you take advantage of the market’s long-term growth while avoiding the pitfalls of trying to time your investments perfectly.”

Conclusion

“Starting your investment journey early can set you up for a financially secure future. Remember, it’s not about getting rich quickly; it’s about making smart, long-term decisions. By understanding the basics of investing, creating a budget, building an emergency fund, and focusing on long-term strategies, you can build a solid financial foundation.”