Let’s be honest who hasn’t dreamed of having enough money saved to tell their job, “See ya!” and start living life on their own terms? Take it from me a dad who’s lived in the States for 18 years I’ve seen how easy it is to get swept up in the ‘American Dream’ without actually saving for the future. Early in my career, I didn’t think much about 401(k) contributions until I nearly missed out on a company match. If you can avoid that mistake, you’ll be miles ahead!

As an NRI, working toward financial freedom by 40 can feel daunting. Between sending money back home, navigating a new culture, and managing daily expenses, saving is an afterthought. But here’s the good news with commitment and smart planning, you can achieve financial independence by the time you’re 40.

Whether you’re fresh out of college or nearing 30, it’s not too late to take control of your finances. This guide breaks down the journey into key phases, with practical, actionable steps to help you grow your wealth. As you go along, you’ll see financial independence isn’t some faraway fantasy it’s an achievable goal.

So, what’s the first step you can take? Reflect on your current financial habits what’s working, and what can be improved. Excited? Let’s get started!

Phase 1: Building a Millionaire Roadmap (Ages 25–28)

The Key Goals:

Your 20s are the perfect time to lay a solid financial foundation. As a dad who started small in his 20s, I get it saving might not seem urgent when you’re just starting your career. But trust me, small, consistent steps during these years can create massive benefits later. Let’s focus on three key goals to set yourself up for success:

Make it your mission to:

- Grow your salary consistently through promotions and raises.

- Save up an emergency fund to cover 6 months of expenses.

- Start investing through retirement and long-term accounts.

Salary and Contributions:

Let’s look at income first. Say you land a job paying $85,000 annually. With about 3% annual raises and occasional promotions, by 28, you could be making around $94,685 yearly. After taxes and deductions, your monthly take-home is roughly $5,000.

Between managing expenses in the U.S. and sending money to family back home, budgeting as an NRI can be tricky. Effective planning ensures you’re steadily progressing toward early retirement goals.

Here’s a sample monthly budget:

| Category | Amount ($) |

| Housing (Rent) | 1500 |

| Transportation (Car) | 250 |

| Groceries | 600 |

| Utilities & Internet | 200 |

| Phone & Insurance | 150 |

| Entertainment | 250 |

| Remittance to Family | 1000 |

| Investments | 550 |

| Emergency Fund | 500 |

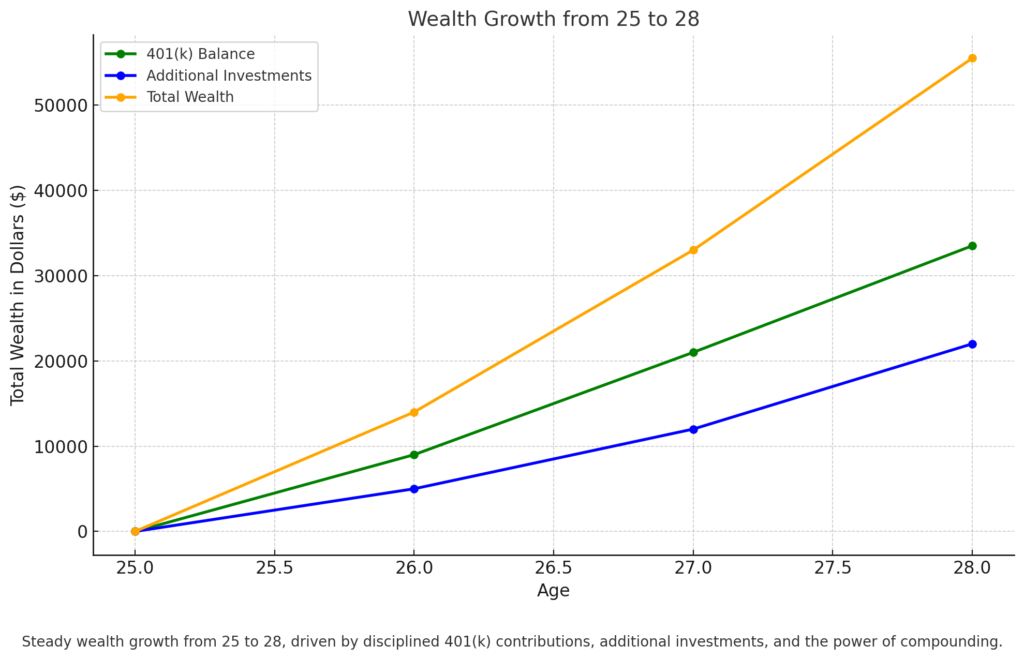

What You Can Achieve by Age 28

By sticking to a plan like this, you could reach the following milestones:

- $33,500 in your 401(k) (including employer match).

- $22,000 in low-cost stock index funds.

- $55,500 in total wealth.

The chart below visualizes the steady growth in wealth during the Foundation Years, showcasing how consistent contributions and compounding investments set the stage for long-term financial success.

It might not seem like a lot yet, but trust me these early years are critical. Small, steady contributions and the power of compounding will create long-term success.

Practical Steps for Your 20s

- Maximize your employer’s 401(k) match: If your employer offers matching contributions, make sure to contribute enough to get the full match. It’s free money you don’t want to miss. Try to contribute at least $10,200 per year, including the employer match.

- Build your emergency fund: Unexpected expenses whether in the U.S. or back in India are inevitable. Having a cash buffer of 6 months’ expenses provides peace of mind. Aim to set aside about $500 per month until you reach this target.

- Start investing early, even in small amounts: Contribute $550 per month to low-cost, diversified index funds. This gives you broad exposure across hundreds of stocks and bonds, keeping risk manageable while letting your money grow steadily over time.

Quick Win:

A close friend of mine started investing just $100 a month at 25. He thought it wasn’t much, but by 30, he was amazed at how much it had grown thanks to compounding. Lesson learned? It’s never about how much you start with it’s about starting, period.

Quick Action:

Take 10 minutes today to review your budget. Where can you cut $50–$100 to boost your investments or savings? Small changes now can lead to big results later.

Key Insight Recap:

- Focus on habits: Building financial habits in your 20s lays the groundwork for long-term success.

- Don’t stress about small beginnings: Every little bit you save or invest will compound over time.

- Stay consistent: By age 28, you’ll have a strong financial base for the next phase of your journey.

Phase 2: Scaling Investments & NRI Wealth-Building Strategies (Age 29–31)

At this stage, your focus shifts from just building a foundation to scaling your investments. Let me share what worked for me during this period of my life. By now, you’ve probably settled into your career, your income is rising steadily, and you’re feeling more confident about managing your finances.

But I know how it feels there are still obligations back home, from supporting parents to sending remittances. Balancing those responsibilities with growing your investments can be challenging, but it’s definitely achievable.

Salary & Contributions:

By this phase, your salary could increase from $97,526 at 29 to $105,474 by 31, thanks to raises and promotions. With a higher income, you can increase your investment contributions to $1,050 per month, ensuring your savings grow alongside your earnings.

Here’s a suggested budget for this phase:

| Category | Amount ($) |

| Housing (Rent) | 1,800 |

| Groceries | 800 |

| Entertainment | 300 |

| Investments | 1,050 |

| Emergency fund | 300 |

| 401(k) Contribution | 1,000 |

| Travel Fund | 500 |

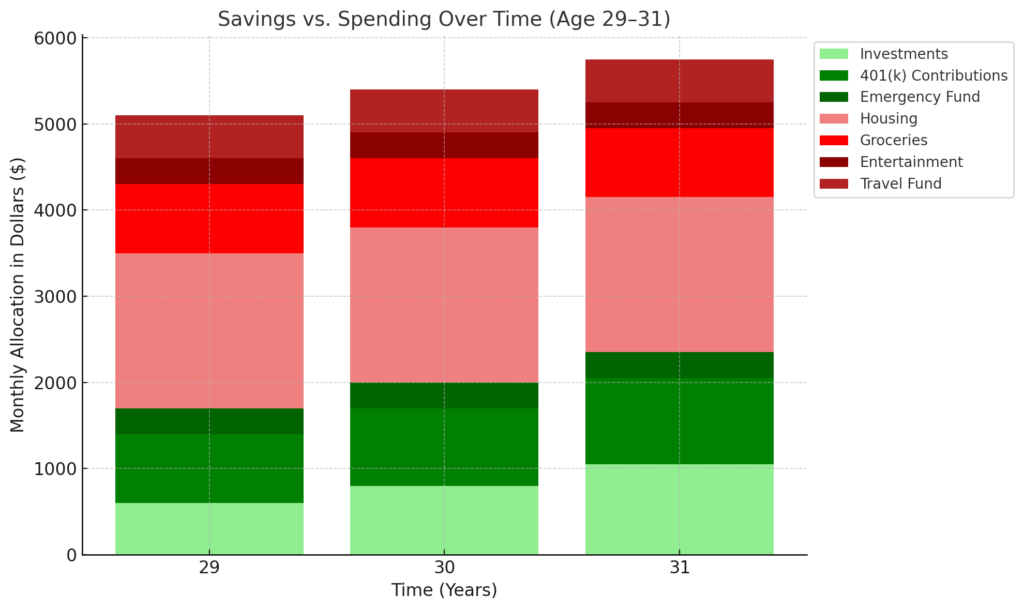

With consistency, here’s what your finances could look like by age 31:

- $89,000 in your 401(k).

- $62,000 in other investments.

- $151,000 in total wealth.

The chart below illustrates the proportional growth in savings versus spending during this phase, highlighting the disciplined approach needed to scale investments effectively:

Proportional growth in savings and investments compared to stable expenses during the Growth Phase (Age 29–31).

How to Scale Your Investments During This Phase:

- Increase 401(k) Contributions:

As your salary increases, aim to contribute 15–20% of each paycheck to your 401(k). This way, you’re fully utilizing the tax advantages and building a robust retirement fund. - Rebalance Your Portfolio:

Since your accounts have grown, now is a good time to reduce your risk slightly. Consider adding 10% in bonds or other stable assets for better protection during market fluctuations. - Enjoy Life Too:

Don’t forget to have some fun along the way. Set aside $500 per month in a travel fund, so you can explore new places without dipping into your retirement savings.

Quick Win:

A colleague of mine started increasing his 401(k) contributions by just $50 every six months. He didn’t even notice the difference in his paycheck, but over time, this small habit added significantly to his retirement savings. Lesson: Small adjustments can lead to big results.

Quick Action:

Take a few minutes this week to look at your budget. Could you cut back on a small expense like eating out or subscriptions and redirect that money toward investments? Even $50–$100 extra per month can make a difference.

Key Insight Recap:

- As your income grows, scale your investments accordingly.

- Don’t overlook the importance of rebalancing your portfolio to manage risk.

- It’s okay to enjoy life budgeting for travel or leisure helps keep you motivated on this journey.

Phase 3: Power Couple Years & Generational Wealth Planning (Age 32–37)

If you’re married or in a committed relationship, this phase is a golden opportunity to leverage dual incomes. My wife and I used this stage to accelerate our savings and investments while preparing for family expenses, and it truly transformed our financial journey.

For many NRIs, this period comes with both opportunities and challenges childcare, education costs, and maintaining financial support for family back home. The key is to balance growing wealth with thoughtful planning for upcoming expenses.

Key Goals for This Phase

- Maximize Household Income

Work as a team to increase income through promotions, raises, or side gigs. A dual income gives you the flexibility to save aggressively. - Continue Scaling Investments

Direct a larger portion of your income into long-term investments, such as 401(k) contributions, stock market investments, or real estate. - Plan for Family Costs

Begin preparing for expenses like childcare, education, or college savings. The earlier you start, the easier it will be to manage these milestones.

Sample Budget for Dual-Income Households

Here’s how a typical monthly budget might look during this phase:

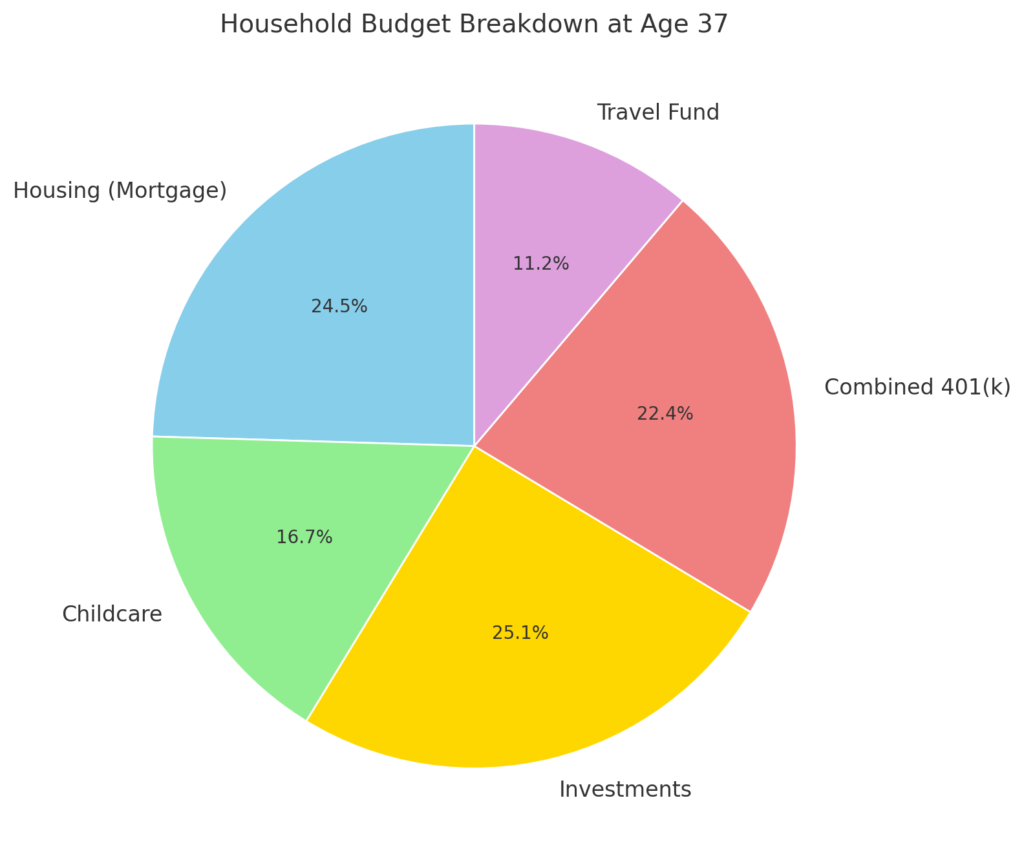

| Category | Amount ($) |

| Housing (Mortgage) | 2,200 |

| Childcare | 1,500 |

| Investment | 2,250 |

| Combined 401(k) | 2,000 |

| Travel Fund | 1,000 |

The pie chart below visually represents this household budget, showcasing how resources are allocated during this critical phase:

Caption: “Household Budget Breakdown for a Dual-Income Family During the Power Couple Years (Age 32–37).”

Wealth Milestones by Age 37

By following a disciplined approach, here’s what you could achieve by 37:

- $320,000 in 401(k) accounts.

- $340,000 in other investments.

- $660,000 in total wealth.

With careful planning, your investments will continue to grow while leaving room for enjoying life and supporting your family.

Some Recommendations During This Stage:

- Avoid Lifestyle Inflation

As income grows, it’s tempting to increase spending on luxuries. Stay disciplined channel extra income into investments rather than unnecessary expenses. - Diversify Your Portfolio

With more assets, it’s important to spread risk. Allocate funds across index funds, individual stocks, and bonds to balance growth with stability. - Save for Education

If you have kids (or plan to), consider a 529 college savings plan. It’s a tax-advantaged way to invest in your child’s future without derailing your other financial goals. - Build a Strong Emergency Fund

With greater responsibilities, aim to save 6–12 months of expenses. This provides security in case of unexpected life changes like job loss or family emergencies.

Quick Win:

When my wife and I started planning for our first child’s education, we realized we needed a dedicated savings plan. Setting up a 529 plan gave us peace of mind and helped us stay on track without sacrificing other goals.

Quick Action:

This week, sit down with your partner to review your finances. If you haven’t already, start a 529 plan, check your portfolio for diversification, and decide how much more you can contribute to savings or investments.

Key Insight Recap:

- Use your dual income to accelerate savings, but avoid lifestyle inflation.

- Diversify your portfolio to protect your growing wealth.

- Plan ahead for big upcoming costs like education and family milestones.

Phase 4: Peak Earnings & Financial Freedom by 40 (Age 38–40)

By your late 30s, you’ve worked hard to build wealth, and now it’s time to protect it. This phase is about making smart, final moves to secure your financial freedom. For NRIs, this often includes preparing for children’s education, supporting elderly parents back home, and managing estate planning across borders. Balancing these responsibilities isn’t easy, but with careful planning, you can confidently approach the next chapter.

Projected Household Income and Expenses:

By this phase, your household income may reach $265,225 annually, but expenses are likely higher too. A typical monthly budget might look like this:

| Category | Amount ($) |

| Housing (Mortgage) | 2,500 |

| Childcare | 3,000 |

| Investments | 3,250 |

| Combined 401(k) | 3,000 |

| Education Savings | 500 |

Final Wealth by Age 40:

Thanks to your disciplined approach over the years, here’s what your wealth could look like by age 40:

- $520,000 in 401(k) savings.

- $580,000 in other investments.

- Total wealth: $1.1 million.

At this point, you have options: retire early, continue working, or pursue personal passions while enjoying financial freedom.

Key Moves to Make During This Phase:

- Diversify with Real Estate:

Consider shifting up to 5% of your portfolio into real estate. This can provide passive income and further diversify your investments. - Initiate Estate Planning:

Create or update wills and trusts to ensure your assets are distributed as you wish. For NRIs, estate planning across two countries can be complex, so consult a financial advisor with cross-border expertise. - Reduce Risk in Your Portfolio:

As you approach financial independence, it’s wise to reduce overall risk in your portfolio. Reallocate a portion of your high-growth investments into more stable options, such as bonds or dividend-paying stocks. This helps protect your wealth from market volatility.

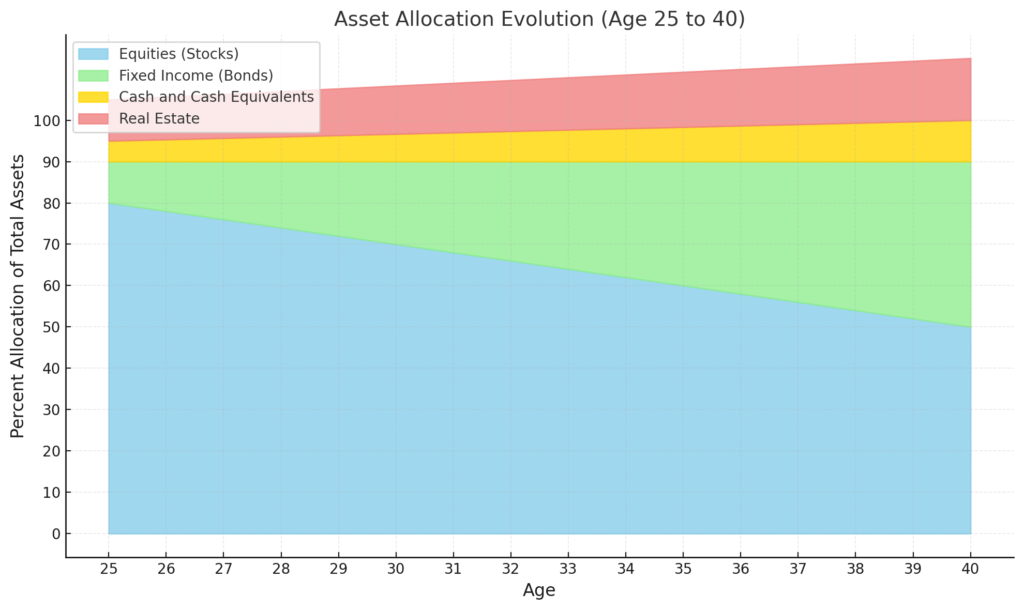

Below is a visual representation of how asset allocation evolves over time, shifting from high-growth investments in your 20s to more stable and diversified allocations by age 40:

Caption: This chart illustrates the evolution of asset allocation from age 25 to 40, showing the gradual shift from equities to a more balanced portfolio focused on stability as financial independence approaches.

Quick Win:

At 40, one of the best decisions I made was consulting a financial advisor about estate planning. It gave me peace of mind knowing my family’s future was secure. The earlier you start, the easier it is to manage.

Quick Action:

Set up a meeting with a financial advisor this month to review your estate plan and diversify your portfolio. Reflect on your current investments: Are they aligned with your long-term goals?

Key Insight:

- Focus on protecting your wealth as you approach financial freedom.

- Diversify into real estate and reduce overall risk in your portfolio.

- Start estate planning early to ensure your assets are well-managed and distributed according to your wishes.

Success Story: Naren & Sugandha’s Journey to Financial Independence

You may have heard stories of people achieving financial independence and quitting their 9-to-5 jobs to focus on their passions. Let me share a real-life example of a couple I know Naren and Sugandha, the story is a perfect example of how smart planning and consistent effort can turn financial independence into reality. Like many Indian immigrants, they dreamed of moving back to India, spending more time with family, and raising their kids in a familiar cultural environment. Achieving this wasn’t easy, but with careful planning, they made it happen.

Here’s how they did it:

- Maximizing Their Income:

During their “power couple” years, Naren and Sugandha prioritized growing their household income. They earned promotions, upgraded their skills, and occasionally took on side gigs. Over time, their annual income grew from $160,000 to $200,000 by their late 30s. - Disciplined Investing:

Naren and Sugandha became serious about investing. They allocated 70% of their portfolio to low-fee index funds, which tend to perform well over time. Another 20% went into stocks in companies they believed in, while the final 10% was invested in bonds for stability. Their disciplined approach paid off, growing their net worth to over $1 million by the time they were ready to retire early. - Planning for Their Children’s Future:

Despite the high costs of raising children in the U.S., they prioritized saving for their kids’ education. They opened a 529 college savings plan, which helped them invest for their children’s future in a tax-advantaged way. Knowing their kids’ education was covered gave them peace of mind. - Adopting a Minimalist Lifestyle:

One of their smartest decisions was embracing a minimalist lifestyle. By cutting unnecessary expenses and focusing on essentials, they built an emergency fund covering 18 months of living costs. This gave them flexibility and confidence when they finally decided to move back to India.

Today, Naren and Sugandha share their journey through a financial independence blog, inspiring others to achieve similar success. Their story shows that with dual incomes, disciplined investing, and a clear plan, financial freedom isn’t just a dream it’s entirely possible..

Conclusion

financial independence doesn’t happen overnight, but it’s achievable with consistent effort. Take it from someone who’s been there making smart money moves, even small ones, which can add up to something big over time.

Whether you’re starting fresh in your 20s or catching up in your 30s, adopting strategies tailored to NRIs and staying disciplined can help you reach financial freedom by 40. You don’t need to have it all figured out right now just take that first step today.

Quick Action:

What’s one small action you can take today to move toward your financial goals? Is it reviewing your budget, increasing your 401(k) contribution, or cutting an unnecessary expense? Share your progress with someone you trust and keep the momentum going.

Final Thoughts:

You’re not alone on this journey. I’ve walked this path myself, and I can tell you—it’s worth it. Every small step gets you closer to the life you want for yourself and your family. You’ve got this, and I’m cheering you on every step of the way!